Financial Education Professionals

Financial Education Professionals has been delivering specialist technical training, licensing compliance solutions and CPD to financial workplaces for over two decades. We ensure every program meets evolving regulatory requirements and remains relevant in a rapidly changing environment. With us, you are not just meeting compliance – you are building capability that lasts.

Compliance Training Courses

Regulatory News

-

10 August 2026

ASIC suspends AFS licence of Central Accord Pty Ltd for 6 months

ASIC has suspended the Australian financial services (AFS) licence of... -

10 August 2026

ASIC protects consumers by removing high-risk financial sector participants

ASIC strengthened consumer protection in 2025-26, delivering 150 administrative enforcement outcomes targeting misconduct... -

10 August 2026

ASIC has issued infringement notices totalling $594,000 to three companies...

-

6 August 2026

Stavro D’Amore jailed for misusing nearly $700,000 in Berndale funds

Former Berndale Capital Securities Pty Ltd director Stavro D’Amore will... -

6 August 2026

ASIC suspends AFS licence of CFD issuer GFA Capital Markets

ASIC has suspended the Australian financial services licence (AFS) of... -

6 August 2026

S&P Global reaffirms AAA credit rating

International ratings agency S&P Global has just re‑affirmed Australia’s AAA credit... -

5 August 2026

ASIC launches small business strategy, helping to educate and protect small businesses

ASIC has today launched a refreshed Small Business Strategy, setting out how... -

5 August 2026

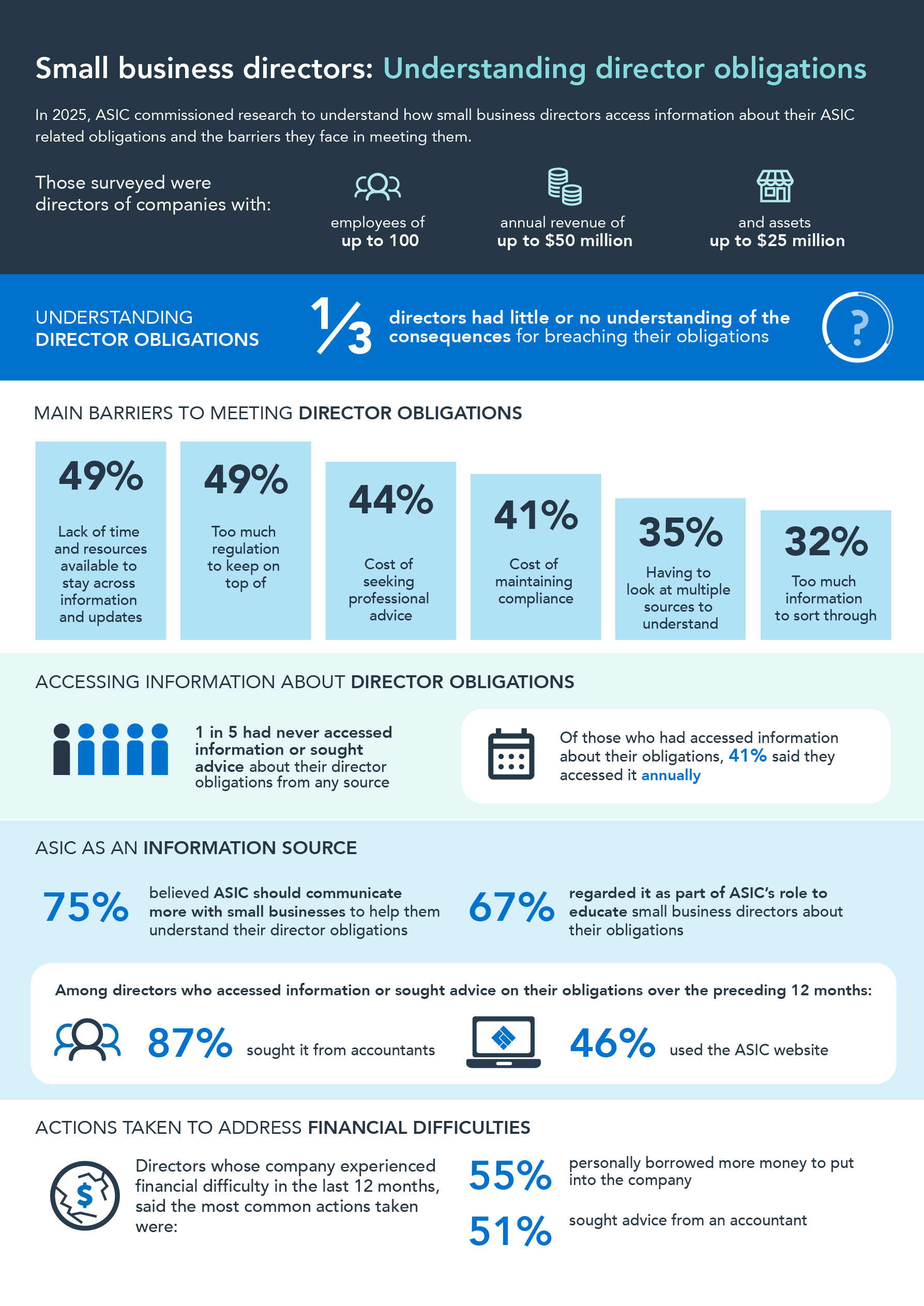

ASIC launches new digital resources for small business directors

ASIC has today launched a new Small Business Director Essentials hub –... -

4 August 2026

ASIC disqualifies Victorian director Antonio Torcasio for 5 years

ASIC has disqualified Antonio Torcasio of Melbourne, Victoria, from managing... -

4 August 2026

ASIC proposes improved pre-IPO advertising flexibility and global alignment

Companies listing on Australia’s public market will have greater flexibility... -

3 August 2026

ASIC acknowledges TMX Group’s acquisition of Cboe Australia

ASIC acknowledges TMX Group Limited’s (TMX) announcement that it has... -

3 August 2026

ASIC is seeking orders from the Federal Court to restrain Royce...

-

3 August 2026

ASIC proposes to remake financial reporting relief for wholly-owned companies

ASIC is seeking feedback on its proposal to remake a... -

30 July 2026

ASIC Chair Sarah Court speaks at Mortgage Offset Press Conference on Wednesday 29 July 2026

Full transcript is available here. -

29 July 2026

Hidden mortgage offset failures costing Australians millions in lost interest savings

Millions of Australians rely on mortgage offset accounts to reduce... -

28 July 2026

Harvey Norman and Latitude ordered to pay combined $55 million penalties for misleading customers

The Federal Court today imposed penalties of $35 million against... -

27 July 2026

APRA releases response to consultation on remaking Level 3 conglomerate standards

The Australian Prudential Regulation Authority (APRA) has released its response... -

24 July 2026

Former director Vickie Anne Vella who used over $1.2 million...

-

24 July 2026

ASIC acts against 36 SMSF auditors, expanding its total enforcement actions this financial year

ASIC took administrative action against 36 approved self-managed superannuation fund... -

23 July 2026

ASIC seeks feedback on remaking low-volume financial market relief

ASIC is inviting industry feedback on its proposal to remake...

Latest Insights

LMI Rethought: Why Lenders Mortgage Insurance is Every Mortgage Broker’s Quiet Superpower

With deposits taking up to 14 years to save, LMI enables earlier home ownership. Discover why brokers should rethink how they position it.

How Do I Become a Responsible Manager?

This back-to-basics guide will help get you started on the path to compliance.

Major Changes to the AML/CTF Regime – Reporting Entities Need to be Prepared

In 2026, a number of significant changes will be made to Australia’s anti-money laundering and counter-terrorism financing (AML/CTF) regime. Are you prepared?