Industry Fundamentals

Essential knowledge about basic principles is learning every financial workplace aspires to uphold. Whether you’re onboarding new starters, maintaining the competence of specialist roles, or seeking reassurance that the whole organisation has your desired level of baseline knowledge, we can meet your needs.

Our range of fundamentals programs:

- Provide new team members helpful information

- Keep specialist roles well-informed and supported

- Equip aspiring leaders to take on new roles

- Deliver company-wide professional development.

Need help finding the right course?

What others say about us

Regulatory News

-

1 May 2026

Former director of collapsed retail over-the-counter derivatives provider Berndale Capital...

-

30 April 2026

APRA finalises targeted amendments to CPS 230 Operational Risk Management

The Australian Prudential Regulation Authority (APRA) has finalised targeted amendments... -

30 April 2026

APRA calls for a step-change in AI-related risk management and governance

The Australian Prudential Regulation Authority (APRA) has called for a... -

29 April 2026

Are you ready for sustainability reporting?

ASIC and the Australian Accounting Standards Board (AASB) will host... -

29 April 2026

Over the last two months, the following enforcement outcomes were...

-

29 April 2026

Updates to OTC derivative clearing and reporting rules

Clearing entities should familiarise themselves with ASIC’s remade over-the-counter (OTC)... -

27 April 2026

Federal Court orders Money3 to pay $1.55 million penalty for responsible lending breaches

The Federal Court has ordered Money3 Loans Pty Ltd (Money3)... -

24 April 2026

APRA consults on amendments to reporting standards for life insurers

The Australian Prudential Regulation Authority (APRA) has released a consultation... -

24 April 2026

ASIC continues finfluencer crackdown alongside global regulators

ASIC is working alongside 16 global regulators as part of... -

23 April 2026

ASIC bans former MWL financial adviser John Morgan for 5 years

ASIC has banned Sydney based former financial adviser John Morgan... -

23 April 2026

eSafety and OAIC working together to protect privacy and safety for all Australians

eSafety and the Office of the Australian Information Commissioner (OAIC)... -

22 April 2026

Regulating cash distribution services

Government released draft legislation to regulate the cash distribution sector... -

20 April 2026

ASIC consults on regulatory guide updates to implement financial market infrastructure reforms

ASIC is advancing the implementation of the Government’s financial market... -

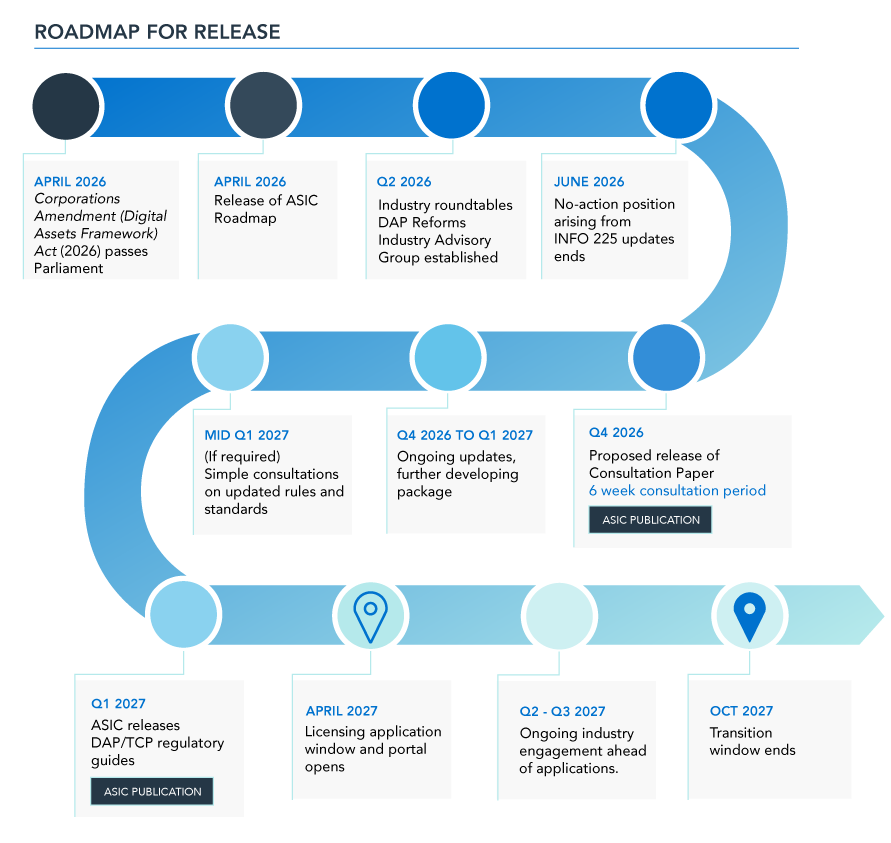

20 April 2026

ASIC’s roadmap for digital assets law reform implementation

ASIC intends to issue new regulatory guidance and set out... -

17 April 2026

Former Beacon Minerals project manager Alexander McCulloch pleads guilty to insider trading

Alexander John McCulloch, a former project manager at Beacon Minerals... -

17 April 2026

The Federal Court has ordered Cigno Australia and its director...

-

15 April 2026

Unacceptable blind spot: low reporting in wealth management sector

AUSTRAC has raised concerns about alarmingly low suspicious matter reporting... -

14 April 2026

Banks step up to disrupt illicit tobacco profits

AUSTRAC has acknowledged the decisive action Australia’s banks have taken... -

13 April 2026

From anxiety to action: Helping Australians to plan for their financial future

ASIC has today launched a new range of free and... -

10 April 2026

ASIC bans former financial adviser Rhys Reilly for 10 years and suspends Conexus Group’s AFS licence

ASIC has banned former financial adviser Rhys James Rolls Reilly...